The Ohio Federation of Academics is accusing KIPP Columbus of working with a “union-busting persuasion campaign” as the constitution school’s workers attempt to unionize.

The campaign has concerned required and voluntary conferences with “anti-union consultants” and a pay a visit to from KIPP’s new CEO Shavar Jeffries, in accordance to OFT President Melissa Cropper.

“Public training funding really should be employed to teach Ohio learners. It should not be used to persuade and intimidate employees who are doing exercises their lawfully safeguarded appropriate to manage a union,” Cropper stated.

KIPP Columbus obtained at least $15 million in general public funding for the 2021-22 faculty yr, which signifies the greater part of its funding, union organizers reported.

“It is incumbent on KIPP to expend that funding on instruction, not union-busting,” Cropper claimed. “If KIPP needs to claim that they are paying out for their union-busting via a diverse source of funding, we sense that is basically a shell sport.”

“We believe that that unfair labor techniques have happened, and we may file official costs on that,” Cropper explained. “Now, we are contacting on KIPP to do the suitable detail and permit their workforce to have a magic formula ballot union election without having intimidation and anti-union lobbying from administration.”

The Dispatch requested KIPP Columbus officials to address the allegations of union-busting, but they did not answer to people precise questions in their prepared reaction.

“We are encouraging all of our colleagues to look at all pertinent details — from many sources — about what it could indicate to be part of a union and what the collective bargaining course of action involves,” KIPP Columbus mentioned in a statement. “Many of our colleagues have questioned thoughts about these subjects, and we are doing work diligently to make certain that all those questions are answered immediately.”

Zach Usmani, a social worker at KIPP elementary and a member of the organizing committee, said the anti-union consultants didn’t share their names through the two-hour meeting he was expected to go to.

“It looks really odd that they really do not want to share any information,” Usmani reported. “It tends to make me problem what’s heading on. Folks are now even far more disappointed for the reason that they are acquiring pulled from their college students to go to these conferences.”

KIPP Columbus did not response The Dispatch’s query as to who the consultants are and how much they are costing the university.

KIPP Columbus, which is element of a countrywide network of faculty preparatory faculties, has about 2,000 college students.

Jeffries took about as KIPP’s CEO the initially week of January and visited KIPP Columbus that exact same week, but staff members questioned the reason of his check out.

“He applied this system to once more force anti-union messaging on our employees,” Usmani reported.

Jeffries is organizing a tour of all KIPP regions and has by now been to Atlanta, Boston, New York and Philadelphia, claimed KIPP Basis spokesperson Maria Alcón-Heraux. He also designs to go to Washington, D.C. and New Orleans in the coming months, Alcón-Heraux reported.

“Shavar Jeffries spoke to KIPP Columbus team and college students about his eyesight for more alignment across KIPP areas as we provide instructional excellence and fairness at a country-primary amount,” Alcón-Heraux mentioned of the pay a visit to in this article.

KIPP Columbus Functions initiatives to unionize have been delayed

“While we regard our colleagues’ rights to be a part of a union, we consider that our current product is the ideal way to produce an revolutionary studying ecosystem for students although supporting and empowering our valued academics and workers,” KIPP Columbus claimed in a statement.

Seventy-eight {e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} of KIPP Columbus’ roughly 130-particular person workers signed union playing cards. Union playing cards ended up submitted with the National Labor Relations Board on Nov. 15, but KIPP Columbus hired the Vorys lawful agency, which submitted a lawful problem with the NLRB on Nov. 16, which has delayed a secret-ballot union election. An NLRB election will not be scheduled right up until the authorized challenge is fixed, which could just take months, Cropper explained.

KIPP Columbus began in 2008 as KIPP Journey Academy with 50 pupils in the fifth grade at a previous Columbus City Educational facilities constructing in Linden and has due to the fact expanded to its present 150-acre campus at 2900 Inspire Generate on the city’s Northeast Aspect. That campus residences the KIPP Columbus Elementary, KIPP Columbus Principal, KIPP Columbus Center, KIPP Columbus Superior, the KIPP Columbus Battelle Environmental Center, the KIPP Columbus Early Discovering Center, and the KIPP Athletics & Wellness Advanced.

Other Ohio constitution educational institutions unionized

KIPP instructors and workers are unionized at the nonprofit public constitution school’s functions in New York City, Baltimore and St. Louis.

If the union is approved by KIPP Columbus’ educators, it would be the 10th constitution school to be part of the OFT. The other OFT unionized constitution colleges in Ohio are in the Cleveland location: Stepstone Academy in Cleveland, Menlo Park Academy in Cleveland, a few colleges in the Summit Academy chain (Parma, Painesville and Lorain) and four educational institutions in the ACCEL constitution chain.

Superintendent experience is not among the qualifications listed Friday in an advertisement seeking applicants for the job of Nebraska commissioner of education.

But it’s easy to see how someone with such experience might check the boxes on the qualifications list assembled by the Nebraska State Board of Education.

The advertisement calls for applicants with experience “as a visionary educational leader within complex organizations and among varied school districts and settings.”

Members of the board are casting a wide net with the broadly written qualifications posted on the website of the search firm McPherson and Jacobson.

The firm is assisting the board in identifying and screening the candidates.

People are also reading…

Steve Joel, one of the consultants, had cautioned the board about narrowing the qualifications so much that qualified candidates without superintendent experience, such as assistant commissioners in other states, would not apply.

Board members are looking for someone to replace Matt Blomstedt, who resigned Jan. 3.

Under the heading of salary range, the advertisement says, “Competitive salary and comprehensive benefits commensurate with experience.”

The listed characteristics sought by the board include the following:

A track record of successfully building teams and consensus as a servant leader who models high character, honesty, respect and trustworthiness in all interactions.

Effective written, oral and interpersonal communication skills, and a commitment to actively engaging stakeholders at all levels.

A critical thinker and creative problem-solver with a history of successful data-informed decision-making, including policy development and academic achievement.

The demonstrated ability to make difficult decisions and effectively manage the people and multiple priorities of a large organization.

An energetic and hard worker who is committed to continuous professional learning focusing on best practices.

The closing date for applications is March 2. Finalists will be selected the week of March 13, and interviews will take place the week of March 27.

Board members will select the new commissioner the week of April 3. Their intention is to have someone in the job by July 1.

Our best Omaha staff photos & videos of January 2023

The Omaha New Year’s Eve fireworks are reflected in the Missouri River with the Bob Kerrey Pedestrian Bridge in the foreground Saturday.

CHRIS MACHIAN photos, THE WORLD-HERALD

Christine Lustgarten poses her dog, Murray, for a portrait after a walk in the snow at Elmwood Park on Tuesday. Lustgarten says her dog enjoys the snow.

CHRIS MACHIAN THE WORLD-HERALD

The Omaha New Year’s Eve fireworks as viewed with the Bob Kerrey Pedestrian Bridge in the foreground from Council Bluffs, Iowa on Saturday.

CHRIS MACHIAN THE WORLD-HERALD

Large blocks of ice rest on the shore of the Missouri River as an ice jam forms near N.P. Dodge Park.

CHRIS MACHIAN, THE WORLD-HERALD

The sunrise illuminates the ice jam on the Missouri River near N.P. Dodge Park.

CHRIS MACHIAN, THE WORLD-HERALD

An ice jam has started to form on the Missouri River near N.P. Dodge Park.

CHRIS MACHIAN, THE WORLD-HERALD

A plane flies near a frozen Carter Lake early on Friday.

Christine Chapman, co-founder of The College Axis Task, has been an educational advisor since 1995.

For significant school juniors and seniors, the pandemic has been a substantial source of uncertainty and anxiousness as learners approach for their academic and professional futures. Worried about the gaps in university advising and application help during this period of time, Christine Chapman founded The College or university Axis Venture (CAP) in May 2021.

Unlike many other college or university steerage programs, CAP is built to provide students of all socioeconomic backgrounds and does not target distinct populations. “We are a blended system,” Chapman clarifies, “so individuals who can find the money for our companies and people who require monetary guidance obtain the exact same higher-good quality products in little-team settings. This also facilitates the sharing of diverse experiences and suggestions.”

CAP’s systems include things like school procedure workshops and boot camps that deal with every little thing from purposes to resumes, particular statements and essays. The nonprofit also offers a two-night school application retreat in Vermont and is obtaining ready to launch a faculty counseling on line system with video clips and guided tutorials. In addition to its compensated courses, CAP delivers common cost-free resources like college profile critique conferences with a qualified college or university counselor and an on the internet resource library for pupils and mom and dad.

The excellent of its instruction is an additional facet that sets CAP aside, Chapman suggests. “The people providing the program include my colleagues, who are seasoned educational consultants, educators and industry experts who have invested a long time performing in faculty admissions and school or steering counseling settings, and me,” Chapman suggests. “Together we characterize additional than 100 several years of expertise in the field.”

Chapman notes that the college or university admission system has developed increasingly nerve-racking and aggressive, although at the identical time, guidance counselors at general public and personal faculties need to take care of overwhelming caseloads. CAP gives pupils a lot-desired personalized guidance that they may well not have ample access to at their schools, Chapman suggests.

Describing the process of working with students on their school essays, Chapman remarks on how contributors are not accustomed to the significant stage of attention that CAP provides. “It’s impressive mainly because our system will allow for relationship and vulnerability to materialize so a actually genuine piece can evolve,” she says. “That’s the things that lights my soul on fire when I believe about the operate that I do and becoming ready to offer that to any person and every person.”

Considering that launching, CAP has supplied more than 100 cost-free college or university profile evaluate opportunities and granted more than $2,000 in fiscal help in the variety of tuition guidance and classes. Chapman is fully commited to the philosophy that these services need to not be a luxury. “I’d like to give each individual substantial school junior and senior the guidance and empowerment that they ought to have as they get prepared to transition into an undergraduate education or a vocational path or whichever it could be,” she claims. “That is what drove me to get University Axis off the ground.”

Chapman lives and operates in Hopkinton, but CAP also is registered to supply solutions in California, Florida, New York and Texas.

To discover far more about The University Axis Challenge, check out thecollegeaxisproject.org, call 617-823-5403, or electronic mail christine@thecollegeaxisproject.org.

Business Profiles are advertising and marketing capabilities intended to present details and qualifications about Hopkinton Unbiased advertisers.

The Kansas City General public College District will current its revised Blueprint 2030 system tonight.It really is a sequence of prolonged-expression approaches that involve the closure of 10 faculties and numerous other adjustments.The closures will dominate the dialogue when it arrives to any transforming of the extended-time period organizing and method of the university district.The 10 educational institutions in concern will probable be repurposed or transformed for an additional use inside the district.The root of the closures are low enrollment and tons of deferred upkeep. The district thinks it will make their use inefficient and ties up resources that Blueprint 2030 aims to increase.The system phone calls for a discounts of $13.2 million to be repurposed for educational and extracurricular pursuits. KCPS leaders, with the enable of consultants, generated the plan following comparing their methods to other school districts.For illustration, they learned that the Springfield, Missouri College District, with 25,000 students, has much less university properties than KCPS, which has about 14,000 learners.The district claims it hopes to improve the instructional experience and educational results for all college students.Several group conferences very last drop have led to Wednesday’s assembly with the revisions the college district desires to go in advance with in Blueprint 2030. There will be no public remark at the board of schooling headquarters meeting.Kansas City general public educational institutions have a scholar-to-teacher ratio of 16 to 1. Its daily attendance price is 91{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf}.

KANSAS City, Mo. —

The Kansas City Community Faculty District will present its revised Blueprint 2030 prepare tonight.

It’s a collection of very long-phrase methods that incorporate the closure of 10 educational facilities and several other alterations.

The closures will dominate the dialogue when it arrives to any remodeling of the lengthy-expression preparing and approach of the faculty district.

The ten colleges in dilemma will very likely be repurposed or converted for a further use within the district.

The root of the closures are reduced enrollment and heaps of deferred upkeep. The district thinks it makes their use inefficient and ties up means that Blueprint 2030 aims to improve.

The strategy calls for a cost savings of $13.2 million to be repurposed for educational and extracurricular routines. KCPS leaders, with the help of consultants, generated the plan after comparing their means to other faculty districts.

For illustration, they uncovered that the Springfield, Missouri College District, with 25,000 pupils, has much less college structures than KCPS, which has about 14,000 students.

The district states it hopes to enrich the academic encounter and educational outcomes for all pupils.

Numerous local community meetings very last drop have led to Wednesday’s conference with the revisions the faculty district wishes to shift forward with in Blueprint 2030.

There will be no community remark at the board of training headquarters meeting.

Kansas Town public educational institutions have a student-to-teacher ratio of 16 to 1. Its daily attendance price is 91{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf}.

Educational Growth Corporation (NASDAQ:EDUC) Q3 2023 Earnings Connect with Transcript January 5, 2023

Operator: Good afternoon, everybody. And thank you for taking part in present-day meeting connect with to explore Instructional Growth Corporation’s Fiscal and Working Results for its Fiscal Third Quarter and Fiscal 2023 Yr-to-date Benefits. As a reminder, this meeting is being recorded. I would now like to convert the conference around to your host, Steven Hooser, Investor Relations.

Steven Hooser: Thank you, operator, and great afternoon, all people. Thank you for becoming a member of us right now for Instructional Development Corporation’s 3rd quarter and fiscal 2023 yr-to-date earnings phone. On the connect with with me right now are Craig White, President and Chief Govt Officer Heather Cobb, Chief Profits and Promoting Officer and Dan O’Keefe, Chief Economical Officer. Immediately after the market closed this afternoon, the company issued a push release saying its final results for the 3rd quarter and fiscal 2023 calendar year-to-date. The launch is readily available on the firm’s website at www.edcpub.com. Prior to turning to the well prepared remarks, I would like to remind you that some of the statements produced right now will be ahead-seeking and are secured underneath the Private Securities Litigation Reform Act of 1995.

Precise effects may vary materially from people expressed or implied because of to a variety of variables. We refer you to Academic Growth Corporation’s new filings with the SEC for a much more in-depth discussion of the company’s fiscal ailment. With that, I would now like to transform the phone in excess of to Craig White, the firm’s President and Chief Government Officer. Craig?

laptop computer-3087585_1280

Craig White: Thank you, Steven, and welcome anyone to the contact. I will begin modern contact with some normal responses in regard to the quarter then I will move the phone off to Dan and Heather to operate through the financials and offer an update on our product sales and advertising and marketing. Lastly, I will wrap up the simply call with some responses and approach and 2023 outlook. We are pleased with our revenue for the 3rd quarter, especially when in contrast to the former quarter. We proceed to encounter macroeconomic pressures from history inflation resulting in significant meals and fuel costs that have hit the pockets of our concentrate on prospects, which are households with youthful youngsters. To beat these continued pressures like lots of merchants, we provide further discounts to guidance our buyers and extra incentives to energize our product sales drive.

These market choices authorized us to create over $30 million in web profits but did impact our means to travel the base-line. Having stated that, I am happy by our capability to remain worthwhile for the quarter. With that, I will convert the get in touch with about to Dan O’Keefe to deliver a short overview of the financials. Dan?

Dan O’Keefe: Thank you, Craig. Turning to the 3rd quarter, net revenues ended up 30.3 million, a reduce of 14.8 million or 32.8{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} in comparison to 45.1 million in the 3rd quarter previous year, or an increase of 56.2{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} as as opposed to 19.4 million for the duration of the former quarter. The once-a-year decrease is owing to the beneficial gain we observed a calendar year back driven by the pandemic. The quarter-around-quarter raises mostly thanks to the seasonality and also integrated some promotions and incentives. Normal active UBAM product sales consultants totaled 27,100 in contrast to 41,500 in the same period of time a year back, and 26,800 in the prior quarter of this year. Throughout the third quarter, we observed stabilization in the regular energetic variety of consultants. We’ve witnessed our lively advisor stages start out to rebound when our leader level consultants continue being at historically high numbers.

Earnings prior to earnings taxes for the 3rd quarter was . million a minimize of 3.6 million as opposed to 3.6 million recorded in the third quarter of final 12 months. Net earnings for the quarter also totaled zero in contrast to 2.6 million a reduce of 2.6 million. Earnings per share totaled zero in comparison to $.31 on a entirely diluted basis. Now turning to our yr-to-date highlights. We recorded web revenues of 72.8 million a lessen of 46.1 million or 38.8{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} compared to 118.9 million through the same period of time of 2022. The decrease was primarily due to reduce active specialist depend coupled with growing inflation, especially through the very first and 2nd quarters this year. Normal active UBAM product sales consultants totaled 28,700 compared to 47,300 for the first three quarters of 2022.

Last calendar year, we observed inflated quantities continuing from the pandemic when university closures ongoing, and several spouse and children associates worked from household. This yr as schools remained open and families returned to work, we’ve viewed our profits advisor levels begin to normalize. Calendar year-to-date reduction for revenue taxes was $800,000, a decrease of 11.7 million as opposed to 10.9 million for the duration of the very same time previous year. Web yr-to-day reduction totaled 600,000, in contrast to 8.6 million for the to start with half of last yr — for the 1st three quarters of previous 12 months, a lower of 8.6 million. 12 months-to-day decline totaled $.07 in comparison to earnings per share of $.94 from the initial 3 quarters of fiscal 2022 down 107.4{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} on a entirely diluted foundation. To update all people on our performing cash stages, inventory ranges decreased from 67.6 million at the conclude of the 2nd quarter to 64.3 million as of November 30, 2022.

Hard cash generated from our lowered inventory was primarily made use of to pay back down our operating funds line, which finished the quarter at $9 million. We proceed to count on even more stock reductions and operating cash line shell out downs throughout our fiscal fourth quarter and all through fiscal 2024 as we normalize our inventory degrees. And finally, our longstanding dividend software continues to be paused as component of the strategic determination to maintain hard cash, which improves dollars flows by approximately 1 million for each quarter. This concludes the monetary update. I will now turn the call more than to Heather Cobb to speak about gross sales and advertising chances in even more element. Heather?

Heather Cobb: Thank you, Dan. As Craig talked about previously, we continue on to consider sector conditions and make adjustments we truly feel are desired to motivate our income force and interact our clients. We ran many purchaser price cut promotions and product sales incentives throughout the quarter to make sure potent results during our peak seasonal selling period. These marketplace conclusions not only aided us normalize our performing cash, but also hold our commission-based product sales drive engaged. All through the next and third quarters, our profits and advertising groups internally expended substantial attempts executing a rebranding directive for our direct revenue division. We declared the rebranding efforts in June engaged a Tier-1 rebranding agency to support us and concluded and introduced the new name of our direct sales division PaperPie in December.

This new title enables us to improved showcase our complete product or service presenting. Kane Miller Publications, Usborne Guides, SmartLab Toys and Studying Wrap-Ups. PaperPie also lets us to establish a recognizable identify distinctive to our enterprise. Our rebranding procedure was concluded before this 7 days, when we transitioned our shopper dealing with ecommerce, and manufacturer husband or wife facing again office to the new paperpie.com. We are very fired up about our new name PaperPie, as it does enable us to establish a recognizable model and encompassing all of our wonderful products and solutions and people today. You will find a great deal of which means behind the identify. But all round, we wished our brand to stand for our mission of accumulating for good around literacy and mastering. This is a recently fashioned compound word which we will be defining ourselves.

At PaperPie, paper is our medium of interaction. Irrespective of whether it truly is a board guide, game items, a sequence of chapter publications or innovative exercise. As the entire world carries on to fight for our children’s interest by means of screens and devices, it has never ever felt much more significant for tangible literacy and understanding resources that will feed the creativeness, improve the emotions and nourish the brain of our kids. And when you assume of pie, you think of anything to be gathered all-around one thing to be shared an practical experience really worth savoring. That is just what we feel our solutions are made for, literacy and finding out as a lifestyle. PaperPie is for memory creating, inventive discovering and limitless choices, all inside of the context of togetherness. Alongside with this strategic rebranding, starting off this week, we rolled out our SmartLab Toys product or service line.

These award-profitable theme-primarily based goods, like squishy human overall body, laboratory toys, science lab toys, and our little series present youngsters ages eight and up fingers-on studying alternatives. We be expecting our initial start of 10 products to have an speedy income effect and we system to follow that up with further item releases mid-year this spring and yet another significant release this summertime. This concludes our profits and marketing update. I will change the get in touch with back about to Craig for closing remarks. Craig?

It is likely that many of our followers know that Multi-Level Marketing (“MLM”) company Educational Development Corporation (NASDAQ:EDUC) is one of our most carefully and thoroughly researched stocks. The volume of our research analyses and follow-on comments published on Seeking Alpha over many years is extensive. While the degree to which we have profited from our insights into EDUC’s business is quite limited, we derive satisfaction from knowing that we have helped our followers save and make a considerable amount of money buying, selling and/or shorting EDUC stock over the years through our timely and unimpeachable analysis.

After EDUC’s latest quarterly earnings report published last week, we feel it is critically important to disclose that our opinion of EDUC’s fundamental trajectory has shifted once again. We strongly recommend that investors who own EDUC stock consider selling their shares at prices above $1.00, as we believe that the company’s latest disclosures reveal even more dramatic problems with its business than we had thought. While we are no longer convinced that there is a large risk of EDUC going out of business in the near-term, we do believe that its earnings power is nowhere near where it once was. While some readers have accused us of vacillating on our opinion of the stock, we believe that it is important as an investor not to be pusillanimous and to be open to changing one’s opinion when presented with new facts.

Summary of Monocle Accounting Research’s Opinions

Before diving in to EDUC’s latest earnings report, we feel that it is important to summarize our latest salvo of public comments and articles over the past eighteen months:

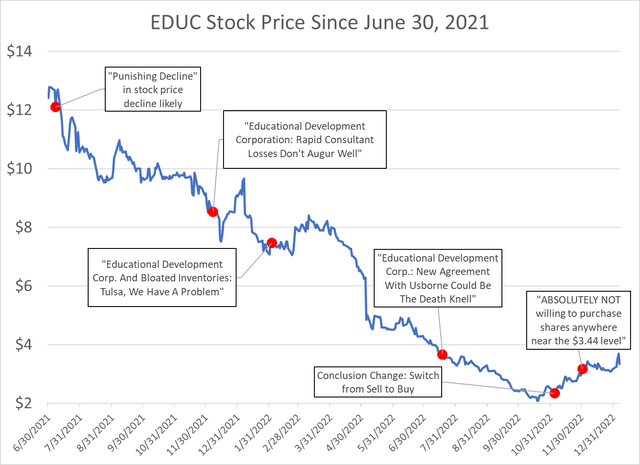

On July 7, 2021, in response to a bullish article by another Seeking Alpha author, we commented that “What will most likely occur with EDUC stock in the coming months is a massive and punishing decline, based on a reduction of active UBAM sales consultants and negative top-line growth.”

On December 6, 2021, Seeking Alpha published our article entitled Educational Development Corporation: Rapid Consultant Losses Don’t Augur Well wherein we stated that “EDUC’s stock price decline throughout 2021 should continue, as investor disappointment over negative growth trends will persist.”

On February 2, 2022, Seeking Alpha published our article entitled Educational Development Corp. And Bloated Inventories: Tulsa, We Have A Problem wherein we warned investors about EDUC’s inventory and other issues, and concluded that “EDUC stock [would] continue to fall meaningfully, as revenues and profits shrink in the quarters ahead”.

On July 14, 2022, Seeking Alpha published our article entitled Educational Development Corp.: New Agreement With Usborne Could Be The Death Knell wherein we questioned the near-term viability of the company due to concerning developments in EDUC’s relationship with its primary supplier, Usborne Publishing.

On November 3, 2022, in a postscript to our Death Knell article, we disclosed how we had changed our opinion on both the viability of EDUC’s business as the near-term future of EDUC stock, as there was evidence that EDUC’s consultant count had stopped its nauseating decline.

And finally, on December 6, 2022, we followed up on our previous comment by stating that we no longer thought EDUC’s stock price reflected good value and opining that the company was fairly valued at $2.50 to $2.75 per share.

EDUC’s stock price since 6/30/21 (Yahoo! Finance; Monocle Accounting Research)

Our intent in enumerating our past opinions about EDUC’s business and stock is not to gloat about the veracity of our information or the accuracy of our predictions, but to provide readers who are unfamiliar with our work with some context as we detail in the coming paragraphs our latest analysis and prediction.

Third Quarter Earnings Report

On Thursday, January 5, EDUC released its earnings report for the company’s fiscal third quarter, ending November 30, 2022, and the numbers, in our opinion, were horrendous.

Every year going back to the mid-1990’s at least, EDUC’s fiscal third quarter has been the company’s strongest revenue quarter of the year. This makes sense considering the school year starts in September and considering EDUC’s end customers buy a lot of books in the months leading up to Christmas. Over the last decade for example, EDUC’s fiscal third quarter has averaged more than a third of the company’s full-year revenue, and more than half of its full-year operating earnings.

This year, EDUC’s third quarter net revenue fell 33{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} year-over-year and its operating income fell an astonishing 94{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf}. In fact, the company’s miniscule operating income of $213,000 was 75{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} lower than the company’s worst third quarter showing in the last twenty years!

And things are likely only going to get worse in the near term. Over the last decade, EDUC’s fourth fiscal quarter ending February has seen net revenue 36{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} lower, on average, than the third quarter. Therefore, without knowing anything further, investors know that the upcoming earnings report is likely to be breathtakingly bad.

But things are likely much worse than normal. Much, much worse…

Publishing Segment

Even though the company did not disclose this within its earnings report on Thursday or during its earnings conference call held later in the day, it did reveal something quite unexpected in its financial statements the following day which should be jarring for holders of EDUC stock.

In its 10-Q filing, EDUC disclosed that “Usborne’s products sold within the Publishing Division accounted for 85.6{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} and 89.2{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} of all products sold during the three and nine months ended November 30, 2022, respectively”. While this sentence is not very well written, we take this to mean that 85.6{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} of the Publishing segment’s Q3 net revenues were related to Usborne products. This is critically important, as EDUC will no longer be entitled to sell Usborne products through its Publishing division effective February 1.

EDUC’s disclosure means that over the last three quarters, EDUC averaged a mere $600,000 in revenue per quarter of Kane Miller products in its Publishing segment.

In our July 2022 article, we said that “EDUC’s Publishing segment’s operating income has typically been a very significant contributor to the company’s overall earnings. EDUC will still get to sell products from its Kane Miller subsidiary as well as other vendors, so it’s not like the Publishing segment is disappearing; however, we believe it is fair to conclude that this segment’s annual operating income figures will be quite a bit lower than what they have been historically.” Well, now that EDUC has disclosed that almost all of its Publishing revenues come from the Usborne product line that it will no longer be able to sell, we believe that EDUC’s Publishing segment is effectively going to be disappearing.

Goodbye to Any Thought of a Dividend Reinstatement

On November 3, 2022, we stated that we believed “EDUC should now be back in a position of experiencing positive free cash flow, and is likely both to reinitiate quarterly dividends (our guess: $0.05 per share per quarter initially) and to restart share repurchases in the very near future.” This statement was based on our assessment of EDUC’s financial condition at the time, and was generally consistent with EDUC’s CEO Craig White’s own public statement on May 12, 2022 when he said a dividend reinstatement is “likely to be third quarter. So we’ve missed the second quarter and be back in the third quarter.”

It is now clear to us that this likely will not be the case.

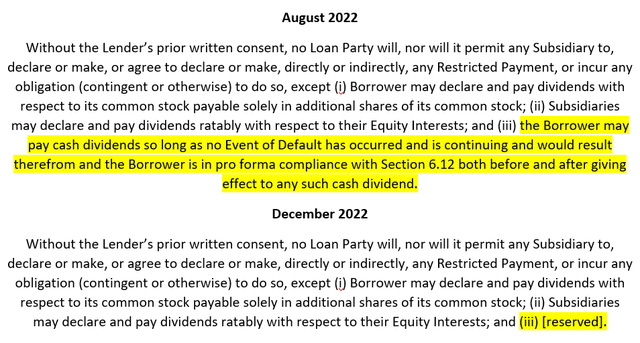

In its latest 10-Q filing, EDUC disclosed that on December 22, 2022, several sections of its Credit Agreement with the Bank of Oklahoma were amended just four months after executing its credit agreement with the bank. First, subsection (a) of Section 6.08 Restricted Payments; Certain Payments of Indebtedness was revised as follows:

A reader unfamiliar with how legal agreements are constructed and revised might think that the highlighted subsection has been amended and redacted, but in fact what the “[reserved]” notation means is that the text in subsection (iii) has been removed in its entirety but the subsection itself has been maintained. This is done so that other sections within the agreement that refer to this subsection do not need to be revised.

In other words, EDUC’s lender appears to be worried enough about the company’s financial state that it has eliminated the ability of EDUC to pay cash dividends.

If one has any doubt about the Bank of Oklahoma’s level of concern, consider also that a new Section 5.01 (1) was just added to the agreement that requires EDUC to furnish to the bank “within 30 days after the end of each calendar month (commencing with the month ending December 31, 2022), [EDUC’s] consolidated and, if applicable, consolidating balance sheet and related statements of operations, all certified by a Responsible Officer of [EDUC] as presenting fairly in all material respects the financial condition and results of operations of [EDUC] and its consolidated Subsidiaries on a consolidated basis in accordance with GAAP consistently applied, and otherwise in a form and in detail reasonably satisfactory to [the bank].”

Consultant Count

In past articles, we have discussed ad nauseam why we believe investors are overestimating EDUC’s UBAM (n/k/a PaperPie) active consultant count from the numbers EDUC discloses to investors. Our concerns continue. For instance, last week, we downloaded the names of over 1,000 PaperPie consultants from the company’s publicly-available website, and based on our proprietary surname analysis (discussed extensively in our previous articles), it appears to us to there are only ~16,500 – 17,000 active consultants at the present time. This is a lower number than we were coming up with just one month ago, and a dramatically lower number than EDUC’s disclosure that it averaged 27,100 active consultants in the third quarter.

Quite frankly, we do not believe investors are getting an accurate view from EDUC’s disclosures of this KPI.

One datum that supports our concern that investors are not getting the full view from EDUC’s management in this regard is the average net revenues per consultant per quarter. This number has steadily fallen over the years, seasonally adjusted. For instance, in EDUC’s third fiscal quarter this year, 27,100 consultants were responsible for net revenue of $25.5 million, or $939.21 per sales consultant. This is down 24{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} from just four years ago.

Valuation and Conclusion

We do not believe eventual bankruptcy is off the table for EDUC. However, we are optimistic by nature and do see a path for EDUC to remain in business for several years at least. In fact, the introduction of toys and games to the company’s product line through its recent acquisition of SmartLab Toys should provide some incremental near-term excitement for the company’s sales organization. As well, the rebranding of UBAM to PaperPie should, despite the curious name choice, give the company’s PaperPie consultants (n/k/a “Brand Partners”) something to talk about.

Given the new information that was disclosed last week though, we have come to the conclusion that EDUC’s stock is worth significantly less than the current stock price.

We will spare our readers the minutiae of our earnings model, but we can summarize our thoughts as follows. We believe that EDUC will be able to average approximately 18,000 PaperPie Brand Partners over the long-term, and we believe annual sales per brand partner will average approximately $3,000. While in the past we had thought that EDUC would generate a significant amount of revenue from its Publishing segment, we now believe that this segment will be eliminated in the near future. As a result, EDUC’s annual revenues should normalize around the $54 million level.

EDUC continues to be wildly overinventoried, and this situation will continue for many quarters to come. This will result in a high level of promotional activity that will depress the company’s operating margin like it did in the latest quarter. However, longer-term, we believe it is reasonable to expect an after-tax profit margin of 2.0{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf} – this belief is rooted in a detailed analysis of the company’s cost structure. On $54 million in sales, that works out to a normalized net income number of $1.08 million.

Considering both the nature of EDUC’s MLM business, the company’s highly indebted balance sheet, the dearth of cash dividends, and the lack of transparency from the company’s current management team, we believe investors will eventually apply a multiple of 8.0x on EDUC’s normalized earnings. This results in a fair value of $1.00 per share. Note that this is considerably below EDUC’s book value per share, and we are very comfortable with this – EDUC’s book value is only relevant in a liquidation scenario, and if EDUC did get liquidated at some point, it is tangible book value that matters.

Based on our current beliefs then, we would be sellers of EDUC stock at prices above $1.00 per share, and buyers of EDUC stock at prices below $0.50 per share.

Risks To Our Thesis

There exists a number of risks that our thesis is incorrect. For instance:

The introduction of products from SmartLab Toys could result in an increase in sales per PaperPie Brand Partner, an increase in the rate of PaperPie Brand Partner recruitment, or both;

EDUC’s credit agreement with Bank of Oklahoma could be amended again to allow for cash dividends; and,

EDUC could cut its operating costs much more than we expect, allowing for its normalized net profit margin to exceed 2.0{e4f787673fbda589a16c4acddca5ba6fa1cbf0bc0eb53f36e5f8309f6ee846cf}.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q3 2023 Earnings Call Transcript")

")